THE ACADEMY OF ECONOMIC STUDIES

MASTER DAFI

I.

The Balanced Scorecard concept

The

Balanced Scorecard concept was first developed during a one year multi company

study - "Measuring Performance in the Organization of tomorrow" sponsored by

Nolan Norton Institute, the research arm of KPMG. The study was motivated by

the need to investigate if that time existing performance-measurement

approaches, primarily relying on financial accounting were preventing the

organizations to create a real economic value.

The

group discussions and the case studies about innovative measurement systems

already implemented in other companies (Analog Devices, 1987) led to the

development of a new supervision method called "Balanced Scorecard". Later on, as

the importance of connecting indicators with a certain strategy or to find the

suitable indicators for a strategy was noticed, the concept extended its applicability

to the strategic management field.

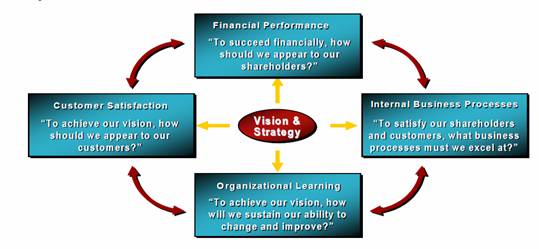

The

Balanced scorecard system analyzes the company from four different

perspectives: the financial perspective, the client perspective, the internal

processes perspective and the learning and development perspective.

The

financial perspective helps to correlate the long term vision of the company

with its financial objectives. In a correct built system each indicator should

be a part of a cause - effect relationship that will result in improving the

financial perspective.

The

client perspective is necessary for identifying potential consumers and the

market segment on which the company should compete. An important criterion for

measurement in this perspective is the market segmentation according to regional

preferences. Nowadays, the customer satisfaction is one of the mandatory

requirements for successful sales.

The

internal processes perspective identifies the critical processes for meeting

the stockholders and the clients' requirements. The objectives and measurements

are defined after the first two perspectives are created in order to be

subordinate to these ones. Important steps in this perspective are innovation,

operational process and the post sales services.

The

efficient usage of BSC forth perspective offers the infrastructure for

obtaining excellent results in the other three perspectives. Kaplan and Norton consider that this

perspective is best defined by three categories of factors: the employees'

abilities, the information systems capacity and the motivation.

To

better understand how the four perspectives are linked to the company's vision

and strategy we can use the map below:

Source: Performance

Management and Balanced Scorecard CFO Services Self - study Guide, Deloitte

Consulting LLP, February 2004

A

Balanced Scorecard should be created when the organization needs a new

performance management system, when a new strategy is necessary or the goals of

the employees and the improvement initiatives should be aligned. The proper organizational unit for a BSC to

be created and implemented is, according to Kaplan and Norton (1996), a

business unit, a unit where we can track and monitor activities related to all

value chain: operations, marketing, services and sales.

In

time, a lot of controversies where engaged over this concept. Its maintainers

praise the BSC ability to:

improve organizational

alignment;

improve external and

internal communication in an organization;

link the operations to

strategy;

to integrate the

planning faze with the strategical management principles;

The

challenges generated by developing and implementing these systems are

considered to be the following:

the lack of an involved

management;

measuring what really

matters;

the belief that BSC is a

short term project ; it is not - it's implementation will change the

organization radically on the long run;

the lack of strategic

thinking;

not taking into account

the whole organizational structure when projecting the system;

The

criticism on the concept can be fought against by using its popularity and

Kaplan and Norton's (1996) arguments. There only is one aspect, in my opinion,

that isn't quite well documented: how can we evaluate the results of a BSC and

check its correctness? The authors

suggest that we should use the strategic feedback feature of the scorecard

developed in the forth perspective in order to track what it's going wrong and

what should be changed. Yet they don't

offer us any receipt to do that.

II.

Techniques used for evaluating the strategy

The

proposed solution will use multicriteria decision methods to hierarchically

arrange the perspectives and the indicators according to their importance in

the eyes of a carefully selected audience. Then we'll calculate the utility

function for each period of time and each factor by using the results in the

timeframes selected. The next step is to picture the factors in an importance -

performance diagram that we'll help us see if we have issues, where the issues

are located and what should we do in order to improve the strategy.

The

method used for the hierarchical arrangement is called AHP - Analytical Hierarchical Perspective. This method offers a

rational framework for structuring a decision problem, for the representation

and quantification of its elements and for linking these elements to the

goals. The problem is decomposed in sub

problems which can be analyzed and evaluated separately. The evaluation can be done using real values

(like quantity, for example) or subjective decisions. These decisions are then

converted into numerical values. A

priority - weight is calculated for each element of the hierarchy, allowing us

to compare elements that differ in signification and measurement method

consistently. The scale used for comparison is the following:

Source: Saaty, Thomas L. (2008-06). "Relative

Measurement and its Generalization in Decision Making: Why Pairwise Comparison are Central in

Mathematics for the Measurement of Intangible Factors - The Analytic Hierarchy/Network

Process".RACSAM (Review of the Royal

Spanish Academy

of Sciences, Series A, Mathematics) 102 (2): 251-318, 257

AHP

proves its efficacy especially when large teams are involved in solving complex

issues that implies hard to quantify elements and long term consequences.

The

method used for calculating utility is called Successive Weighting Method. This method is used to calculate and

differentiate the utilities when we know the weight of each criterion. This

decisional problem is characterized by a consequence matrix:

|

Nature

conditions

|

|

N1

|

N2

|

N3

|

|

Criterions

|

C1

|

|

Cn

|

C1

|

|

Cn

|

C1

|

|

Cn

|

|

Alternatives

|

|

V1

|

a111

|

|

a1n1

|

a112

|

|

a1n2

|

a11r

|

|

a1nr

|

|

V2

|

a211

|

|

a2n1

|

a212

|

|

a2n2

|

a21r

|

|

a2nr

|

|

|

|

|

|

|

|

|

|

|

|

Vm

|

am11

|

|

amn1

|

am12

|

|

amn2

|

am1r

|

|

amnr

|

|

Weights

|

|

|

пn

|

|

|

пm

|

|

|

пr

|

In

order to calculate the utilities we should transform the matrix of consequences

into a utilities matrix. The next step is to normalize the matrix:

rij = aij / ∑ aij , i=1..m, j = 1..n

Each

decisional alternative is associated with a utility function:

f:V→R, f(Vi) = ∑ пj

* rij / ∑ пj i = 1..m

The alternatives are

then ordered in the descending order of the utility functions.

The

graphical representation of factors in relation with their weight and score

(utility) is done by using the Performance - Score analysis. The technique is

based on constructing a score importance diagram split into four quadrants:

Depending

on the quadrant the indicator will fall in, we'll have to follow one of the

four indications.

III.

Balanced Scorecard in organizations. Appling the strategy

and evaluating the results.

In

this case study we'll describe the strategy applied in a department of

Hewlett-Packard and how it's quantified through the BSC concept. We'll then use

the techniques presented in the last chapter to investigate the efficiency of

the strategy on 2008 timeframe.

The

strategic objective at corporation's level is to establish HP as the world's

leading Technology Company. The strategic

framework prepared to sustain this objective is:

Invent and develop

technology solutions for customers;

Drive select industry

trends;

Become the best-in-class

in the industry.

The

operating framework has as objectives: efficiency, targeted growth and capital

strategy.

The

Volume Operations department is a global structure designed to support the

business units on daily basis. The department vision and mission are aligned

with the overall vision and mission. The strategy objectives split omong the

four perspectives of the BSC are the following:

Financial perspective:

Cut costs;

improve the efficiency

of key elements: risk assessment, documentation;

simplifying the business

programs by introducing standardized promotions;

periodic analysis of

prices related to profitability;

support growth on

emergent markets and new business initiatives.

Client perspective:

automatisation of orders

and reducing the time to process the order;

improving delivery time;

standardized procedures for global accounts;

increase customer satisfaction;

reduce the number of disputed invoices.

Internal processes perspective:

standardization and

alignment at global level for configuration , call-center , catalogues and

prices;

using Six Sigma to

optimize costs;

reducing the amount and

value of field inventory;

increasing the number of

orders delivered in the negotiated period of time;

Reducing the number of

claims.

Learning and growth perspective:

improving management

communication;

specialized trainings;

Diversity.

By

applying AHP technique on the indicators chosen to represent these objectives

we obtained a weight for each perspective and for each indicator:

|

Pespective

|

The weight in BSC

|

|

Financial Perspective

|

|

|

Indicator

|

The weight in perspective

|

The weight in BSC

|

|

Employee number

|

|

|

|

Sales turnover

|

|

|

|

Expenses

|

|

|

|

% of time worked per

employee

|

|

|

|

Client Perspective

|

|

|

Indicator

|

The weight in perspective

|

The weight in BSC

|

|

% of electronic

orders

|

|

|

|

Time of completion

|

|

|

|

Disputed invoices

|

|

|

|

Internal Business Perspective

|

|

|

Indicator

|

The weight in perspective

|

The weight in BSC

|

|

Standardised

procedures

|

|

|

|

Six-sigma

certificates

|

|

|

|

Field inventory

|

|

|

|

% standard agreed

time

|

|

|

|

% claims

|

|

|

|

Learning and development perspective

|

|

|

Indicator

|

The weight in perspective

|

The weight in BSC

|

|

Trust in management

|

|

|

|

Carrier plans

|

|

|

|

Specialized trainings

|

|

|

By

applying the Successive Weighting Method, we then determined the utility

functions for each of the timeframes selected: Q1, Q2, Q3 and Q4 for 2008 for

overall strategy and each indicator.

|

Utility functions

|

|

f(Q1)

|

|

|

f(Q2)

|

|

|

f(Q3)

|

|

|

f(Q4)

|

|

The

indicators were represented in an Importance - Score analysis diagram:

According

to the result on this diagram we recommend that the time of completion which is

located in quadrant 1 should be carefully supervised. Also the sales turnover

should be carefully checked because of the economic conjuncture and of their

decrease in the last couple of months. For better results, the cutting costs

policy should also be continued.

The

proposed methods can be used in strategy valuation exercises as well as in

projects designed for optimizing different processes, systems or procedures.

IV.

Bibliography:

Kaplan R S, Norton D P, "The Balanced

Scorecard - Measures that drive performance", Harvard Bussiness School Press, Boston Massachusetts,

1992

Kaplan R S, Norton D P, "Putting the

Balanced Scorecard to Work",, Harvard Bussiness School

Press, Boston Massachusetts,1993

Kaplan R S, Norton D P, "Using Balanced

Scorecard as a Strategic Manangement System" Harvard

Bussiness School

Press, Boston Massachusetts,1996

Kaplan R S, Norton D P, 'The

Balanced Scorecard :translating strategy into action:", Harvard Bussiness

School Press, Boston Massachusetts, 1996

Kaplan R S, Norton D P, 'The

Strategy-Focused Organization: How Balanced Scorecard Companies Thrive in the

New Business Environment", Harvard Bussiness School

Press, Boston Massachusetts, 2000

Kaplan R S, Norton D P, "Double - Loop

Management: Making Strategy a continous process", Harvard Bussiness School

Press, Boston Massachusetts,2000

Niven, Paul R. 'Balanced Scorecard.

Step-by-step. Maximizing Performance and Maintaining Results', John

Wiley&Sons, Inc, 2002.

Kenny, Graham "Balanced Scorecard: Why it

isn't working", Business Performance Measurement, Le Magnus University Press,

2005

Nørreklit, Hanne, "The Balanced

Scorecard: what is the score? A rhetorical analysis of the Balanced Scorecard",

Accounting,Organizations and Society, 2003

Saaty, Thomas L. (2008-06). "Relative

Measurement and its Generalization in Decision Making: Why Pairwise Comparison are Central in

Mathematics for the Measurement of Intangible Factors The Analytic Hierarchy/Network Process".RACSAM

(Review of the Royal

Spanish Academy

of Sciences, Series A, Mathematics) 102 (2): 251-318

Dobre I, Badescu A., Irimiea N.,

Teoria deciziei - studii de caz, Editura Scripta, 2000

Williams, Albert E., Neal, Larry L.,

"Motivational Assesment in Organization: An application of Importance -

Performance Analysis", Journal of Park and Recreation Administration, 1993

Martilla, J.& James J. (1977) Importance

- performance analysis. Journal of marketing,41(1), 77-79

Kendrick J., Saaty D., "Use Analytic

Hierarchy Process for Project Selection", Six Sigma Forum Magazine, 2007

Derringer, Goerge C., "A balancing act:

optimizing a product's properties", Quality progress Magazine, 1994

Mehnen, J, Trautmann H., "Integration of

expert's preferences in Pareto optimization by desirability function

techniques", Intelligent Computation in Manufacturing Engineering, 2000

Harrington J., "The desirability

function. Industrial quality control, 21/10: 494 - 498, 1965

Rohm H., "A balancing act", Performance

measurement in action, Vol. 2, Issue 2,2004

https://people.revoledu.com/kardi/tutorial/AHP

https://www.geocities.com/lbu_measure/qestlime/qestlime.htm

https://ezinearticles.com/?The-Efficient-BSC-For-Management.htm

https://ezinearticles.com/?Components-of-BSC-Analysis.htm

www.balancedscorecard.org